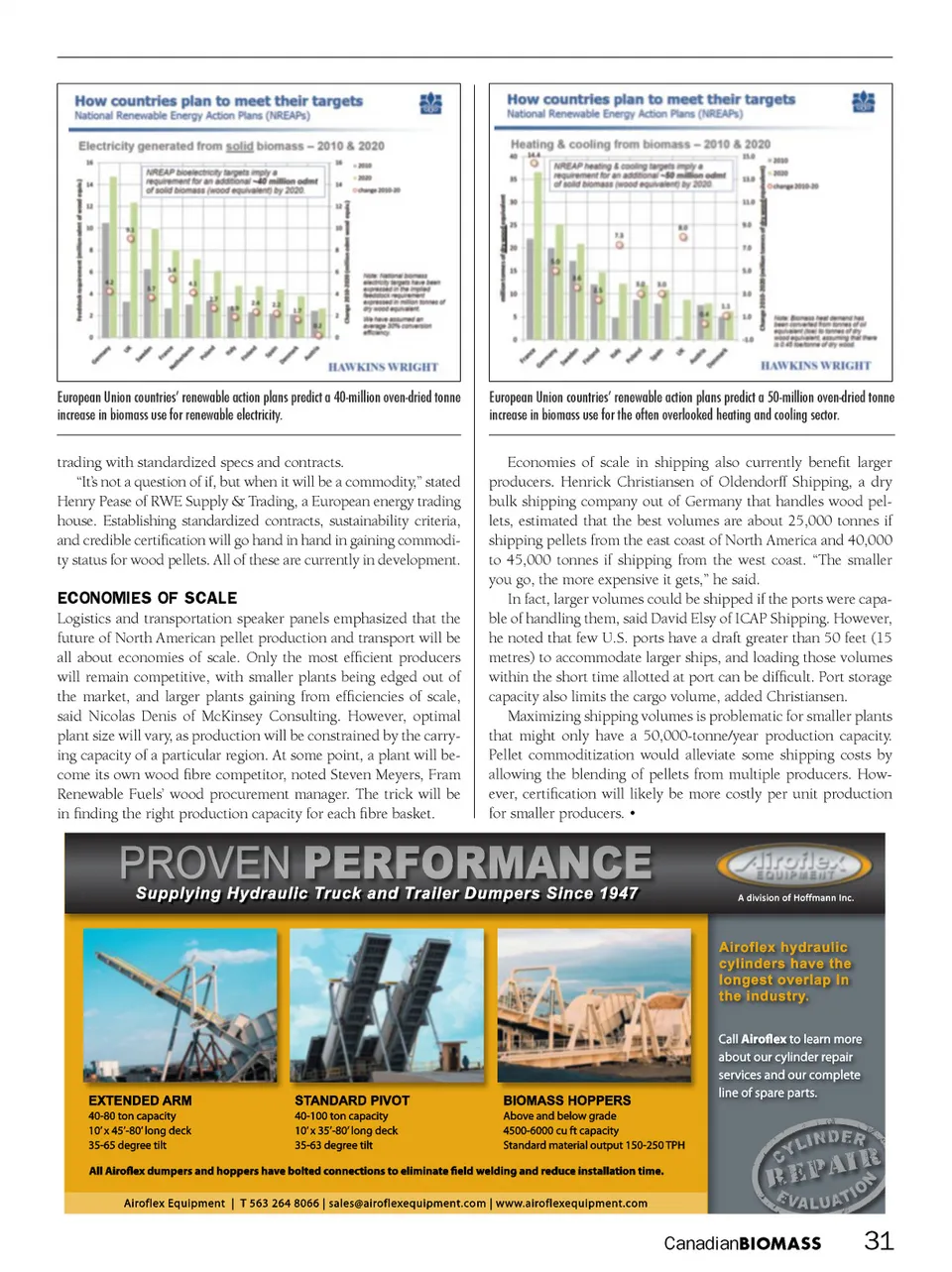

Conference Report Pellet Export Strategies North American pellet producers will have to keep up with market developments to retain access to industrial pellet end-users. By Heather Hager m arkeT consultants expect the global wood pellet industry to triple over the next ten years as renewable energy gains in importance. That potential is already attracting new players to pellet manufacturing, both within and outside North America. To dis-cuss strategies and challenges for moving their wood pellets in the growing global industrial market, North American pellet exporters met in New Orleans in Septem-ber 2011 at the North American Biomass Pellet Export Conference. The increasing demand for pellets will intensify producer competition, par-ticularly with new entrants from low-cost regions outside North America, such as Brazil and Russia, said Jonathan Rager of Pöyry Management Consulting. With the European Union predicted to remain the most important market (and smaller growth in Asia and North America), re-gions of the world that have a sustainable, low-cost fibre supply and short-distance shipping access to Europe should benefit most. Something for North American pel-let exporters to keep an eye on, said Rager, is “where that new supply will go, and how it will affect the existing markets.” “The European Union is still where the game is, from an industrial pellet per-spective,” said John Bingham of UK-based Hawkins Wright, a forest markets consul-tancy. About 90% of EU biomass import demand currently goes to the UK, Nether-lands, Sweden, Denmark, Belgium, and It-aly. Based on EU member countries’ renew-able energy plans, Bingham expects to see growth of 40 million and 50 million oven-Representatives from European utilities and pellet traders kicked off the conference with an overview of current pellet use. From left: Henry Pease of RWE Supply & Trading; Niels Bojer Jørgensen, purchaser for Denmark’s Dong Energy; Simon Rodian Christensen of Copenhagen Merchants; Ben Goh, senior biomass fuel developer for German utility Eon; Nicolas Denis of McKinsey Consulting; and panel moderator Thomas Meth, executive vice-president of U.S. pellet producer Enviva. dried tonnes of biomass for the power and heating markets, respectively, by 2020. Ma-jor growth markets will be Germany, UK, Italy, Sweden, Netherlands, and Poland for power generation, and France, Germany, Italy, UK, and Sweden for heating and cooling. However, Germany, France, and Poland should be able to meet their sup-ply from domestic sources, said Bingham. These markets will continue to be highly dependent on policy direction, he added. key criteria Sustainability was a key buzzword through-out the conference. “Sustainability to bio-mass is like safety to nuclear,” said Ben Goh of Eon, a Germany-based power and gas company. “Utilities must be seen to be acting in a manner consistent with sustain-ability.” With the EU establishing criteria for sustainably harvested biofuels, North American pellet producers are eager to see some final policy direction so they can en-sure their pellets will meet the standards. Currently, a major challenge for pellet producers is that each utility sets its own pellet specifications. Simon Rodian Chris-tensen of Copenhagen Merchants, which ships and handles pellets and owns several port terminals, gave numerous examples. Some power plants require low fines/dust if located near residential areas or if the pellets need to be handled multiple times. Utilities can also differ in requirements for nitrogen level, ash content, and pellet diameter, contract term, shipment size, etc. This means that producers need to understand as many specs as possible and be able to meet them, said Christensen, il-lustrating the need to commoditize pellet SEPTEMBER/OCTOBER 2011 30 Canadian BIOMASS

Canadian Biomass September/October 2011: Page 30