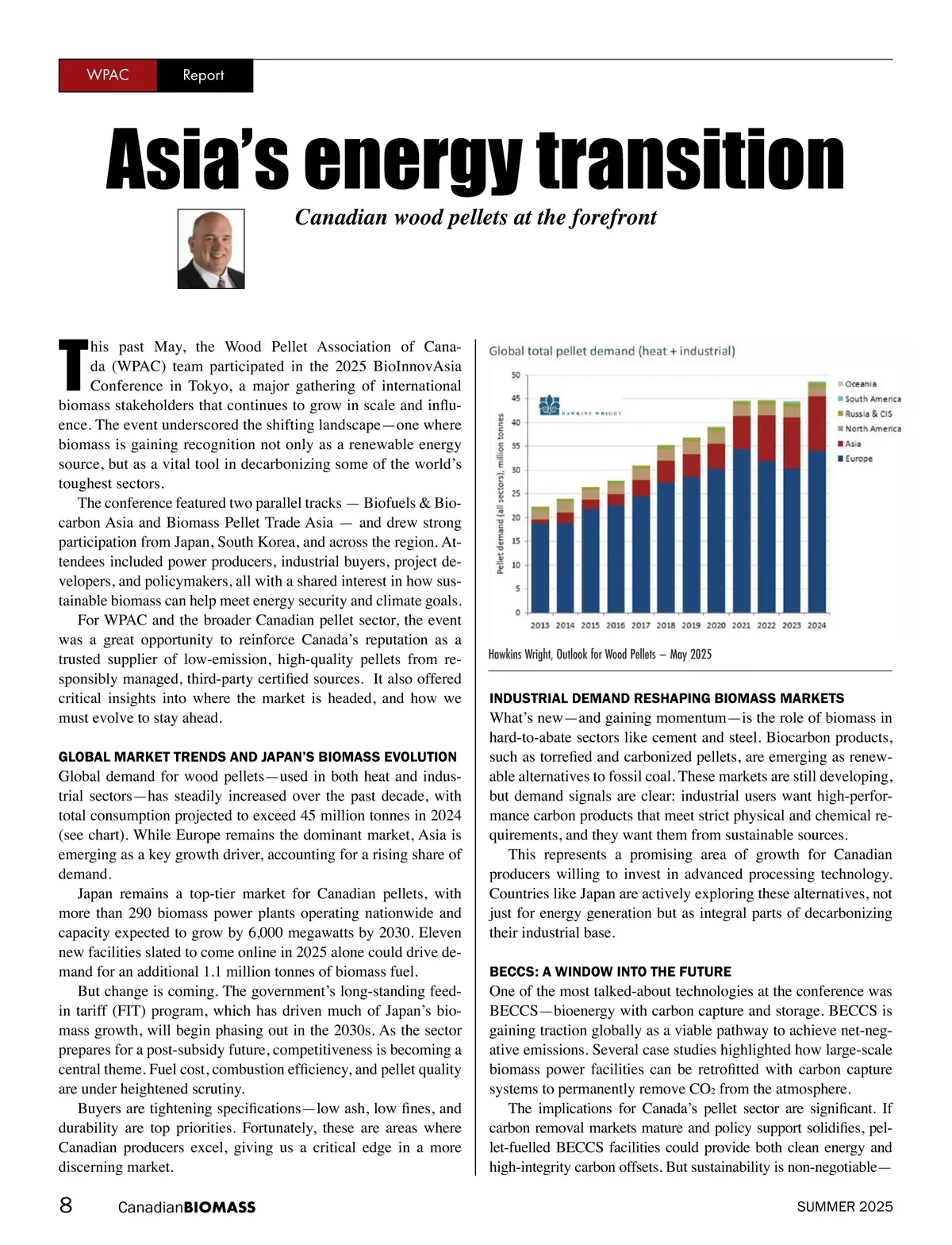

WPAC Report Asia’s energy transition Canadian wood pellets at the forefront T his past May, the Wood Pellet Association of Cana-da (WPAC) team participated in the 2025 BioInnovAsia Conference in Tokyo, a major gathering of international biomass stakeholders that continues to grow in scale and influ -ence. The event underscored the shifting landscape—one where biomass is gaining recognition not only as a renewable energy source, but as a vital tool in decarbonizing some of the world’s toughest sectors. The conference featured two parallel tracks — Biofuels & Bio-carbon Asia and Biomass Pellet Trade Asia — and drew strong participation from Japan, South Korea, and across the region. At-tendees included power producers, industrial buyers, project de-velopers, and policymakers, all with a shared interest in how sus-tainable biomass can help meet energy security and climate goals. For WPAC and the broader Canadian pellet sector, the event was a great opportunity to reinforce Canada’s reputation as a trusted supplier of low-emission, high-quality pellets from re-sponsibly managed, third-party certified sources. It also offered critical insights into where the market is headed, and how we must evolve to stay ahead. GLOBAL MARKET TRENDS AND JAPAN’S BIOMASS EVOLUTION Hawkins Wright, Outlook for Wood Pellets – May 2025 INDUSTRIAL DEMAND RESHAPING BIOMASS MARKETS Global demand for wood pellets—used in both heat and indus-trial sectors—has steadily increased over the past decade, with total consumption projected to exceed 45 million tonnes in 2024 (see chart). While Europe remains the dominant market, Asia is emerging as a key growth driver, accounting for a rising share of demand. Japan remains a top-tier market for Canadian pellets, with more than 290 biomass power plants operating nationwide and capacity expected to grow by 6,000 megawatts by 2030. Eleven new facilities slated to come online in 2025 alone could drive de-mand for an additional 1.1 million tonnes of biomass fuel. But change is coming. The government’s long-standing feed-in tariff (FIT) program, which has driven much of Japan’s bio-mass growth, will begin phasing out in the 2030s. As the sector prepares for a post-subsidy future, competitiveness is becoming a central theme. Fuel cost, combustion efficiency, and pellet quality are under heightened scrutiny. Buyers are tightening specifications—low ash, low fines, and durability are top priorities. Fortunately, these are areas where Canadian producers excel, giving us a critical edge in a more discerning market. What’s new—and gaining momentum—is the role of biomass in hard-to-abate sectors like cement and steel. Biocarbon products, such as torrefied and carbonized pellets, are emerging as renew -able alternatives to fossil coal. These markets are still developing, but demand signals are clear: industrial users want high-perfor-mance carbon products that meet strict physical and chemical re-quirements, and they want them from sustainable sources. This represents a promising area of growth for Canadian producers willing to invest in advanced processing technology. Countries like Japan are actively exploring these alternatives, not just for energy generation but as integral parts of decarbonizing their industrial base. BECCS: A WINDOW INTO THE FUTURE One of the most talked-about technologies at the conference was BECCS—bioenergy with carbon capture and storage. BECCS is gaining traction globally as a viable pathway to achieve net-neg-ative emissions. Several case studies highlighted how large-scale biomass power facilities can be retrofitted with carbon capture systems to permanently remove CO 2 from the atmosphere. The implications for Canada’s pellet sector are significant. If carbon removal markets mature and policy support solidifies, pel -let-fuelled BECCS facilities could provide both clean energy and high-integrity carbon offsets. But sustainability is non-negotiable— SUMMER 2025 8 Canadian BIOMASS

Canadian Biomass Summer 2025: Page 8