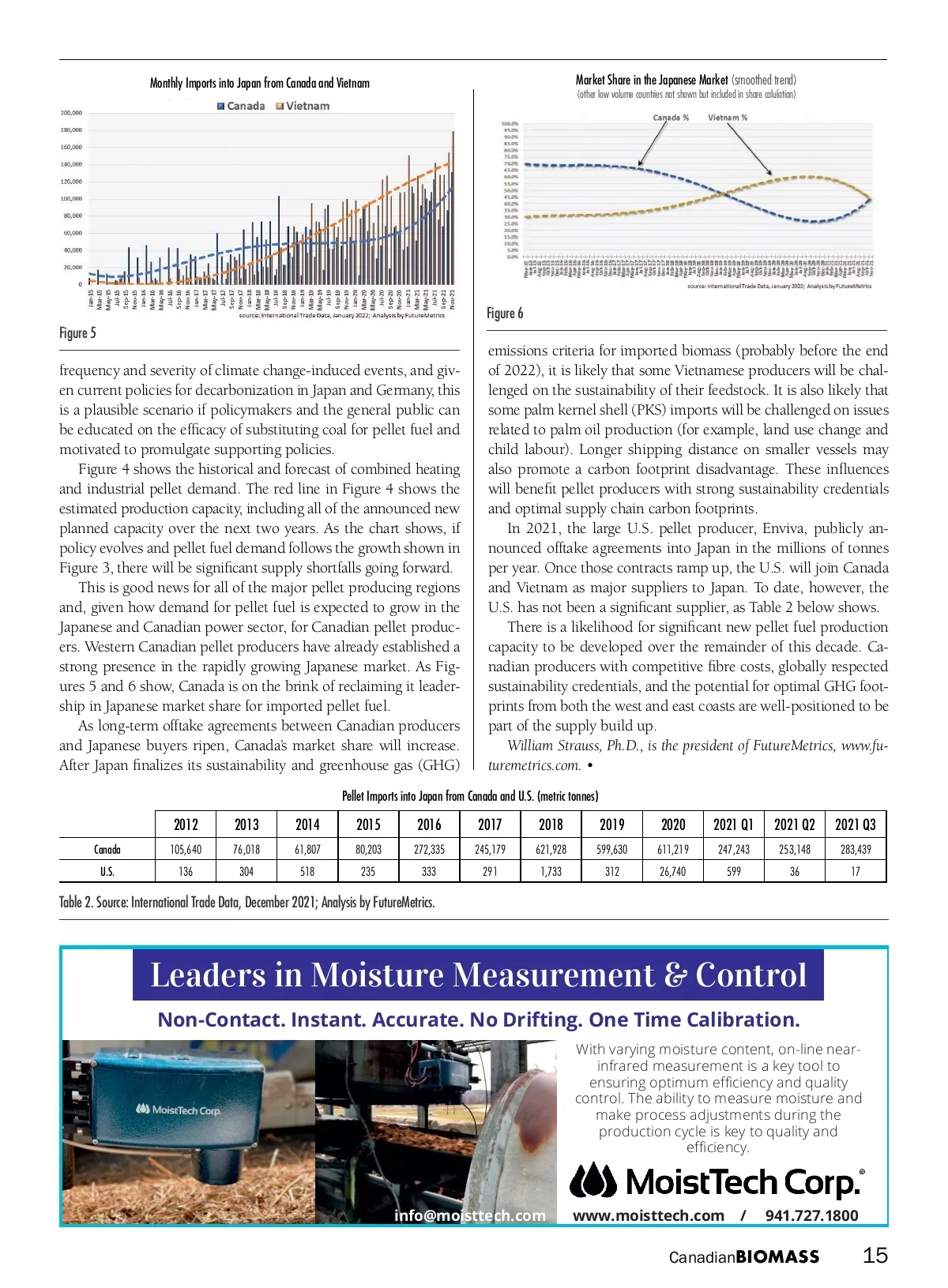

Monthly Imports into Japan from Canada and Vietnam Market Share in the Japanese Market (smoothed trend) (other low volume countries not shown but included in share calulation) Figure 6 Figure 5 frequency and severity of climate change-induced events, and giv-en current policies for decarbonization in Japan and Germany, this is a plausible scenario if policymakers and the general public can be educated on the efficacy of substituting coal for pellet fuel and motivated to promulgate supporting policies. Figure 4 shows the historical and forecast of combined heating and industrial pellet demand. The red line in Figure 4 shows the estimated production capacity, including all of the announced new planned capacity over the next two years. As the chart shows, if policy evolves and pellet fuel demand follows the growth shown in Figure 3, there will be significant supply shortfalls going forward. This is good news for all of the major pellet producing regions and, given how demand for pellet fuel is expected to grow in the Japanese and Canadian power sector, for Canadian pellet produc-ers. Western Canadian pellet producers have already established a strong presence in the rapidly growing Japanese market. As Fig-ures 5 and 6 show, Canada is on the brink of reclaiming it leader-ship in Japanese market share for imported pellet fuel. As long-term offtake agreements between Canadian producers and Japanese buyers ripen, Canada’s market share will increase. After Japan finalizes its sustainability and greenhouse gas (GHG) emissions criteria for imported biomass (probably before the end of 2022), it is likely that some Vietnamese producers will be chal-lenged on the sustainability of their feedstock. It is also likely that some palm kernel shell (PKS) imports will be challenged on issues related to palm oil production (for example, land use change and child labour). Longer shipping distance on smaller vessels may also promote a carbon footprint disadvantage. These influences will benefit pellet producers with strong sustainability credentials and optimal supply chain carbon footprints. In 2021, the large U.S. pellet producer, Enviva, publicly an-nounced offtake agreements into Japan in the millions of tonnes per year. Once those contracts ramp up, the U.S. will join Canada and Vietnam as major suppliers to Japan. To date, however, the U.S. has not been a significant supplier, as Table 2 below shows. There is a likelihood for significant new pellet fuel production capacity to be developed over the remainder of this decade. Ca-nadian producers with competitive fibre costs, globally respected sustainability credentials, and the potential for optimal GHG foot-prints from both the west and east coasts are well-positioned to be part of the supply build up. William Strauss, Ph.D., is the president of FutureMetrics, www.fu-turemetrics.com. • Pellet Imports into Japan from Canada and U.S. (metric tonnes) 2012 Canada U.S. 105,640 136 2013 76,018 304 2014 61,807 518 2015 80,203 235 2016 272,335 333 2017 245,179 291 2018 621,928 1,733 2019 599,630 312 2020 611,219 26,740 2021 Q1 247,243 599 2021 Q2 253,148 36 2021 Q3 283,439 17 Table 2. Source: International Trade Data, December 2021; Analysis by FutureMetrics. Leaders in Moisture Measurement & Control Non-Contact. Instant. Accurate. No Drifting. One Time Calibration. With varying moisture content, on-line near-infrared measurement is a key tool to ensuring optimum efficiency and quality control. The ability to measure moisture and make process adjustments during the production cycle is key to quality and efficiency. [email protected] www.moisttech.com / 941.727.1800 CB_MoistTech_Winter22_CSA.indd 1 Canadian BIOMASS 2022-01-24 1:13 PM 15

Canadian Biomass Winter 2022: Page 15