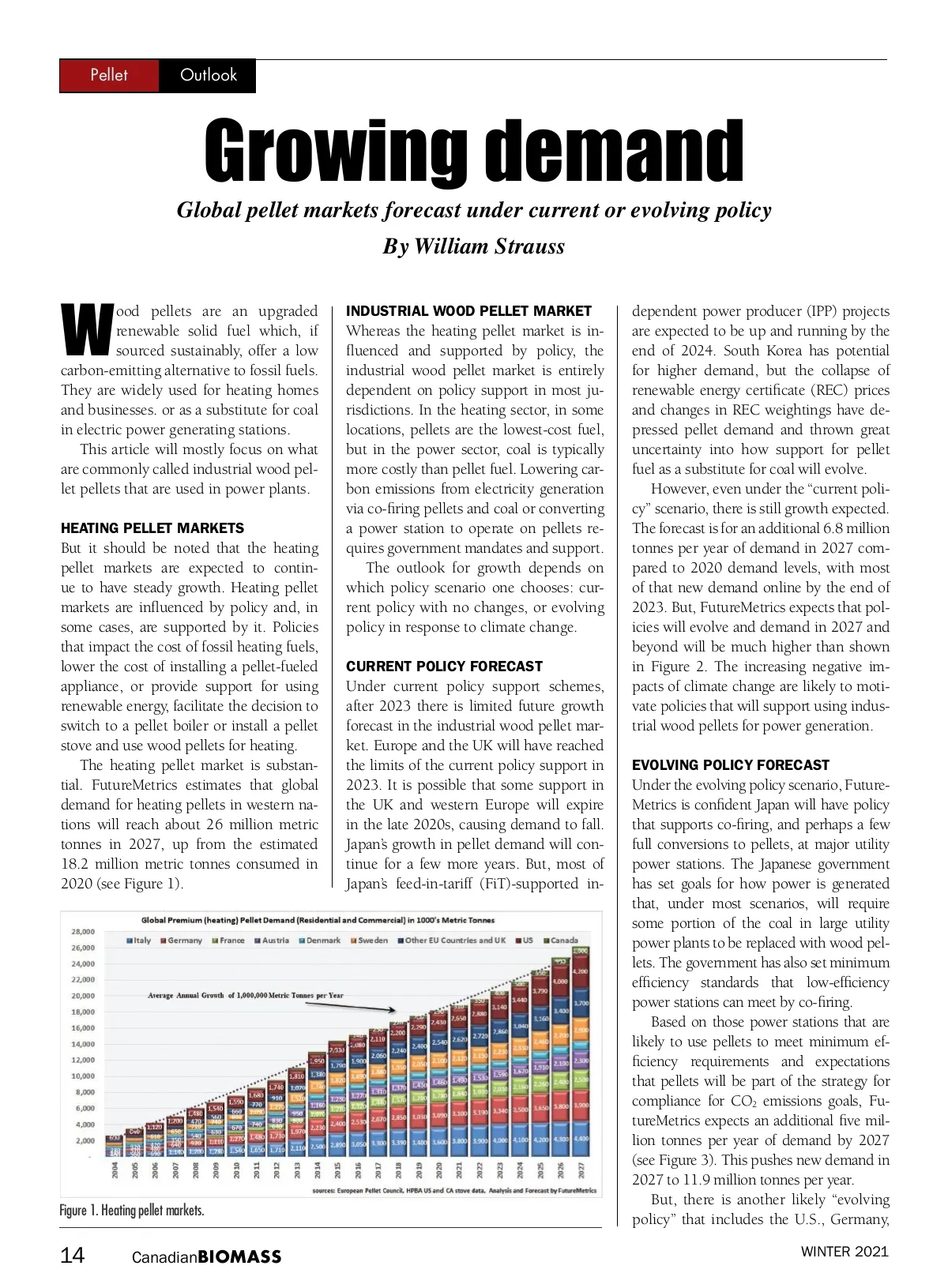

Pellet Outlook Global pellet markets forecast under current or evolving policy By William Strauss Growing demand INDUSTRIAL WOOD PELLET MARKET W ood pellets are an upgraded renewable solid fuel which, if sourced sustainably, offer a low carbon-emitting alternative to fossil fuels. They are widely used for heating homes and businesses. or as a substitute for coal in electric power generating stations. This article will mostly focus on what are commonly called industrial wood pel-let pellets that are used in power plants. HEATING PELLET MARKETS But it should be noted that the heating pellet markets are expected to contin-ue to have steady growth. Heating pellet markets are influenced by policy and, in some cases, are supported by it. Policies that impact the cost of fossil heating fuels, lower the cost of installing a pellet-fueled appliance, or provide support for using renewable energy, facilitate the decision to switch to a pellet boiler or install a pellet stove and use wood pellets for heating. The heating pellet market is substan-tial. FutureMetrics estimates that global demand for heating pellets in western na-tions will reach about 26 million metric tonnes in 2027, up from the estimated 18.2 million metric tonnes consumed in 2020 (see Figure 1). Whereas the heating pellet market is in-fluenced and supported by policy, the industrial wood pellet market is entirely dependent on policy support in most ju-risdictions. In the heating sector, in some locations, pellets are the lowest-cost fuel, but in the power sector, coal is typically more costly than pellet fuel. Lowering car-bon emissions from electricity generation via co-firing pellets and coal or converting a power station to operate on pellets re-quires government mandates and support. The outlook for growth depends on which policy scenario one chooses: cur-rent policy with no changes, or evolving policy in response to climate change. CURRENT POLICY FORECAST Under current policy support schemes, after 2023 there is limited future growth forecast in the industrial wood pellet mar-ket. Europe and the UK will have reached the limits of the current policy support in 2023. It is possible that some support in the UK and western Europe will expire in the late 2020s, causing demand to fall. Japan’s growth in pellet demand will con-tinue for a few more years. But, most of Japan’s feed-in-tariff (FiT)-supported in-dependent power producer (IPP) projects are expected to be up and running by the end of 2024. South Korea has potential for higher demand, but the collapse of renewable energy certificate (REC) prices and changes in REC weightings have de-pressed pellet demand and thrown great uncertainty into how support for pellet fuel as a substitute for coal will evolve. However, even under the “current poli-cy” scenario, there is still growth expected. The forecast is for an additional 6.8 million tonnes per year of demand in 2027 com-pared to 2020 demand levels, with most of that new demand online by the end of 2023. But, FutureMetrics expects that pol-icies will evolve and demand in 2027 and beyond will be much higher than shown in Figure 2. The increasing negative im-pacts of climate change are likely to moti-vate policies that will support using indus-trial wood pellets for power generation. EVOLVING POLICY FORECAST Figure 1. Heating pellet markets. Under the evolving policy scenario, Future-Metrics is confident Japan will have policy that supports co-firing, and perhaps a few full conversions to pellets, at major utility power stations. The Japanese government has set goals for how power is generated that, under most scenarios, will require some portion of the coal in large utility power plants to be replaced with wood pel-lets. The government has also set minimum efficiency standards that low-efficiency power stations can meet by co-firing. Based on those power stations that are likely to use pellets to meet minimum ef-ficiency requirements and expectations that pellets will be part of the strategy for compliance for CO 2 emissions goals, Fu-tureMetrics expects an additional five mil-lion tonnes per year of demand by 2027 (see Figure 3). This pushes new demand in 2027 to 11.9 million tonnes per year. But, there is another likely “evolving policy” that includes the U.S., Germany, WINTER 2021 14 Canadian BIOMASS

Canadian Biomass Winter 2021: Page 14