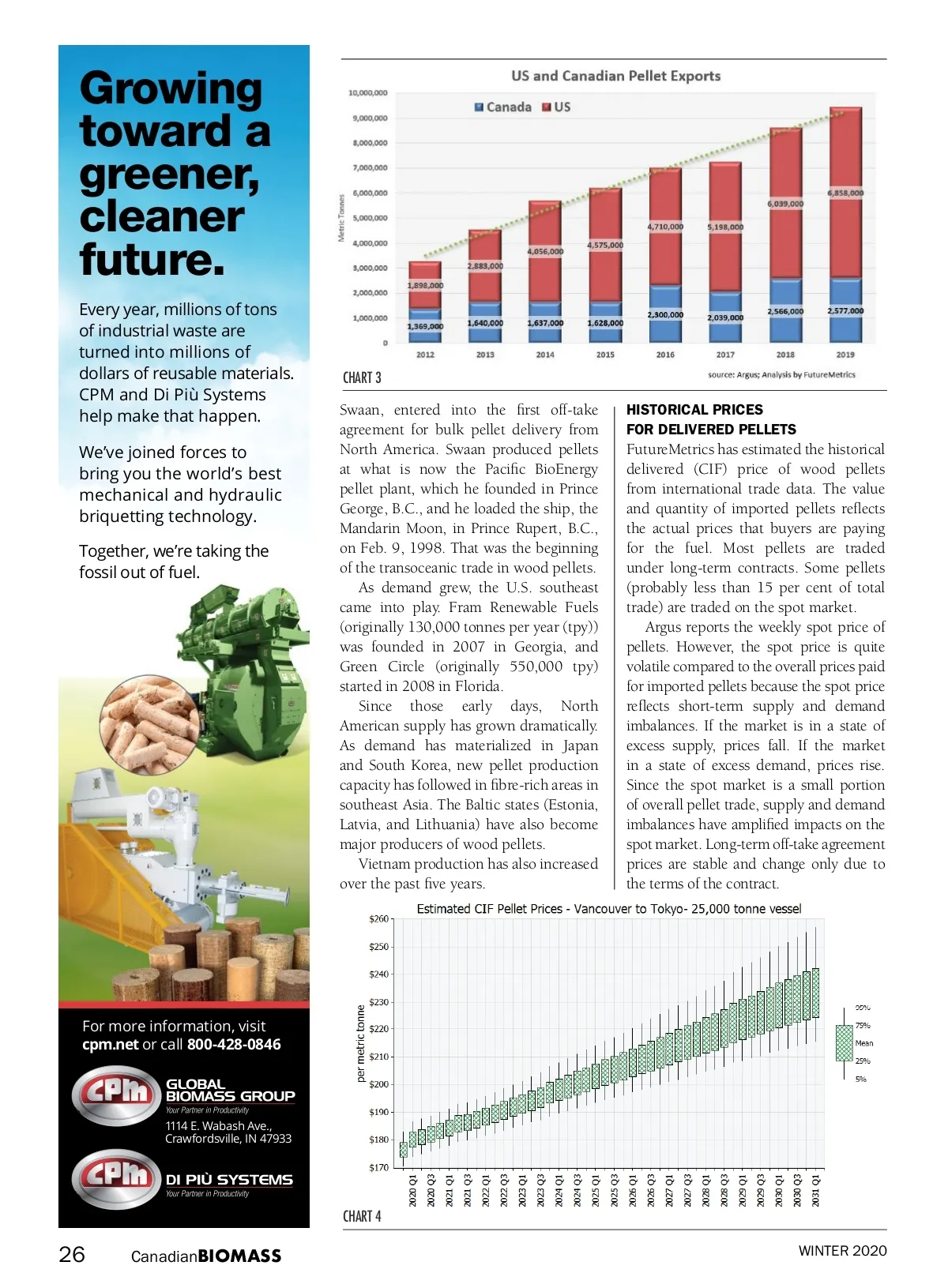

FutureMetrics’ estimates the CIF prices and market shares by major suppliers for the U.K., Japan, and South Korea. Note that monthly data is somewhat volatile in part due to how the data is gathered and the number of shipments per month for any given month. The trade weighted average price and the trend lines help to see through the volatility. Even with those issues, the estimated pellet prices are far less volatile on a three-month rolling average than the spot prices. FUTURE PELLET PRICES? The price of pellets will be heavily influenced by long-term contracts for wood pellets. In fact, as noted above, the volatility of the spot market increases because the majority of the market is under long-term contract. Since such a large percentage of the market is already under long-term take-or-pay contracts, when the market is in periods of excess demand or excess supply, the majority of the market correction has to take place within the 10-20 per cent of the total market that is traded on spot. In the long run, the contract price and spot price should converge around a market equilibrium price. The intrinsic costs of producing and delivering pellets, including typical profit margins, will set the market prices for long-run supply contracts. Many of the forecast model’s modules use oil prices as a significant source of cost uncertainty. Harvesting and transporting wood to pellet mills, conversion to pellets, transport logistics by truck, rail, and ship, all contain a significant exposure to petroleum costs (such as diesel and bunker fuels). FutureMetrics utilizes the United States Energy Information Administration’s (EIA) forecast for oil prices (West Texas Intermediate or WTI). Historical pellet ocean shipping freight rates provide insight into the expected long-term market clearing rates for typical-sized vessels from various pellet export terminals. FutureMetrics does not try to forecast the short-to medium-term drivers of shipping cost volatility. The methodology of estimating expected future CIF prices involves developing independent forecasts for each of the main components of pellet costs: wood costs delivered to the pellet mill; pellet mill conversion costs (excluding wood costs); pellet producers’ expected margins (using EBITDA per tonne as the model input); inland transportation from the mill to the port, and port storage and loading costs; and shipping. Expected EBITDA/tonne is based on historical data from the two publicly traded producers (Pinnacle and Enviva) and from FutureMetrics data based on due diligence analysis on existing pellet plants. Based on a number of assumptions, the forecasted prices for the next 10 years are shown in Chart 4. Find more charts and analysis in the online version of this article at www.canadianbiomassmagazine.ca. • William Strauss, Ph.D., is the president of FutureMetrics. www.futuremetrics.com. Authorized Distributor of Contact Cardinal for all your equipment, parts and service needs! www.cardinalsaw.com [email protected] Follow us Canadian BIOMASS CB_CSEBLISS_FALL2019_ASK.indd 1 CB_Cardinal_Winter20_CSA.indd 1 2019-10-08 1:34 PM 27 2020-02-10 1:27 PM

Canadian Biomass Winter 2020: Page 27