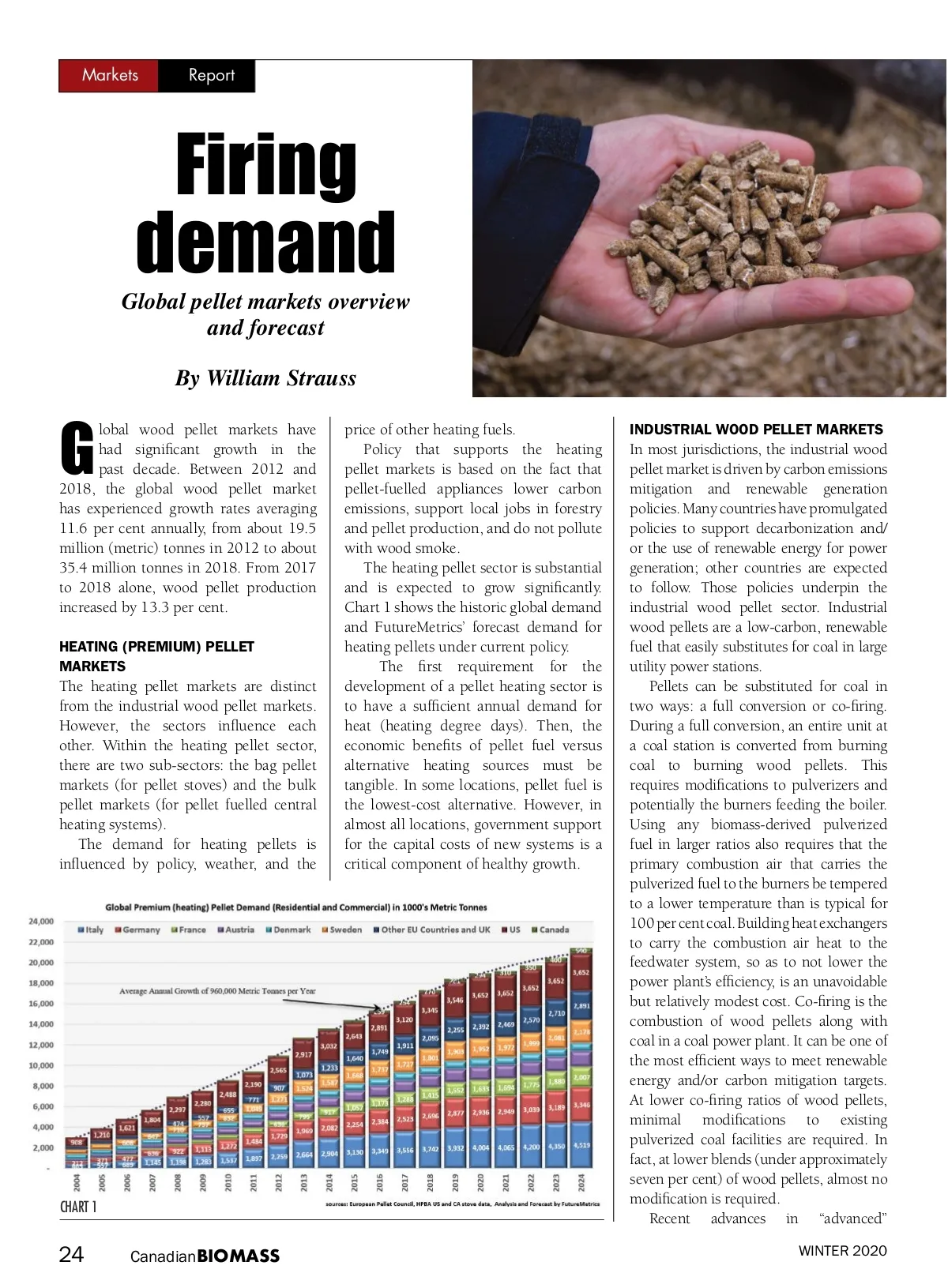

Markets Report Global pellet markets overview and forecast By William Strauss lobal wood pellet markets have had significant growth in the past decade. Between 2012 and 2018, the global wood pellet market has experienced growth rates averaging 11.6 per cent annually, from about 19.5 million (metric) tonnes in 2012 to about 35.4 million tonnes in 2018. From 2017 to 2018 alone, wood pellet production increased by 13.3 per cent. HEATING (PREMIUM) PELLET MARKETS Firing demand G The heating pellet markets are distinct from the industrial wood pellet markets. However, the sectors influence each other. Within the heating pellet sector, there are two sub-sectors: the bag pellet markets (for pellet stoves) and the bulk pellet markets (for pellet fuelled central heating systems). The demand for heating pellets is influenced by policy, weather, and the price of other heating fuels. Policy that supports the heating pellet markets is based on the fact that pellet-fuelled appliances lower carbon emissions, support local jobs in forestry and pellet production, and do not pollute with wood smoke. The heating pellet sector is substantial and is expected to grow significantly. Chart 1 shows the historic global demand and FutureMetrics’ forecast demand for heating pellets under current policy. The first requirement for the development of a pellet heating sector is to have a sufficient annual demand for heat (heating degree days). Then, the economic benefits of pellet fuel versus alternative heating sources must be tangible. In some locations, pellet fuel is the lowest-cost alternative. However, in almost all locations, government support for the capital costs of new systems is a critical component of healthy growth. INDUSTRIAL WOOD PELLET MARKETS CHART 1 In most jurisdictions, the industrial wood pellet market is driven by carbon emissions mitigation and renewable generation policies. Many countries have promulgated policies to support decarbonization and/ or the use of renewable energy for power generation; other countries are expected to follow. Those policies underpin the industrial wood pellet sector. Industrial wood pellets are a low-carbon, renewable fuel that easily substitutes for coal in large utility power stations. Pellets can be substituted for coal in two ways: a full conversion or co-firing. During a full conversion, an entire unit at a coal station is converted from burning coal to burning wood pellets. This requires modifications to pulverizers and potentially the burners feeding the boiler. Using any biomass-derived pulverized fuel in larger ratios also requires that the primary combustion air that carries the pulverized fuel to the burners be tempered to a lower temperature than is typical for 100 per cent coal. Building heat exchangers to carry the combustion air heat to the feedwater system, so as to not lower the power plant’s efficiency, is an unavoidable but relatively modest cost. Co-firing is the combustion of wood pellets along with coal in a coal power plant. It can be one of the most efficient ways to meet renewable energy and/or carbon mitigation targets. At lower co-firing ratios of wood pellets, minimal modifications to existing pulverized coal facilities are required. In fact, at lower blends (under approximately seven per cent) of wood pellets, almost no modification is required. Recent advances in “advanced” WINTER 2020 24 Canadian BIOMASS

Canadian Biomass Winter 2020: Page 24