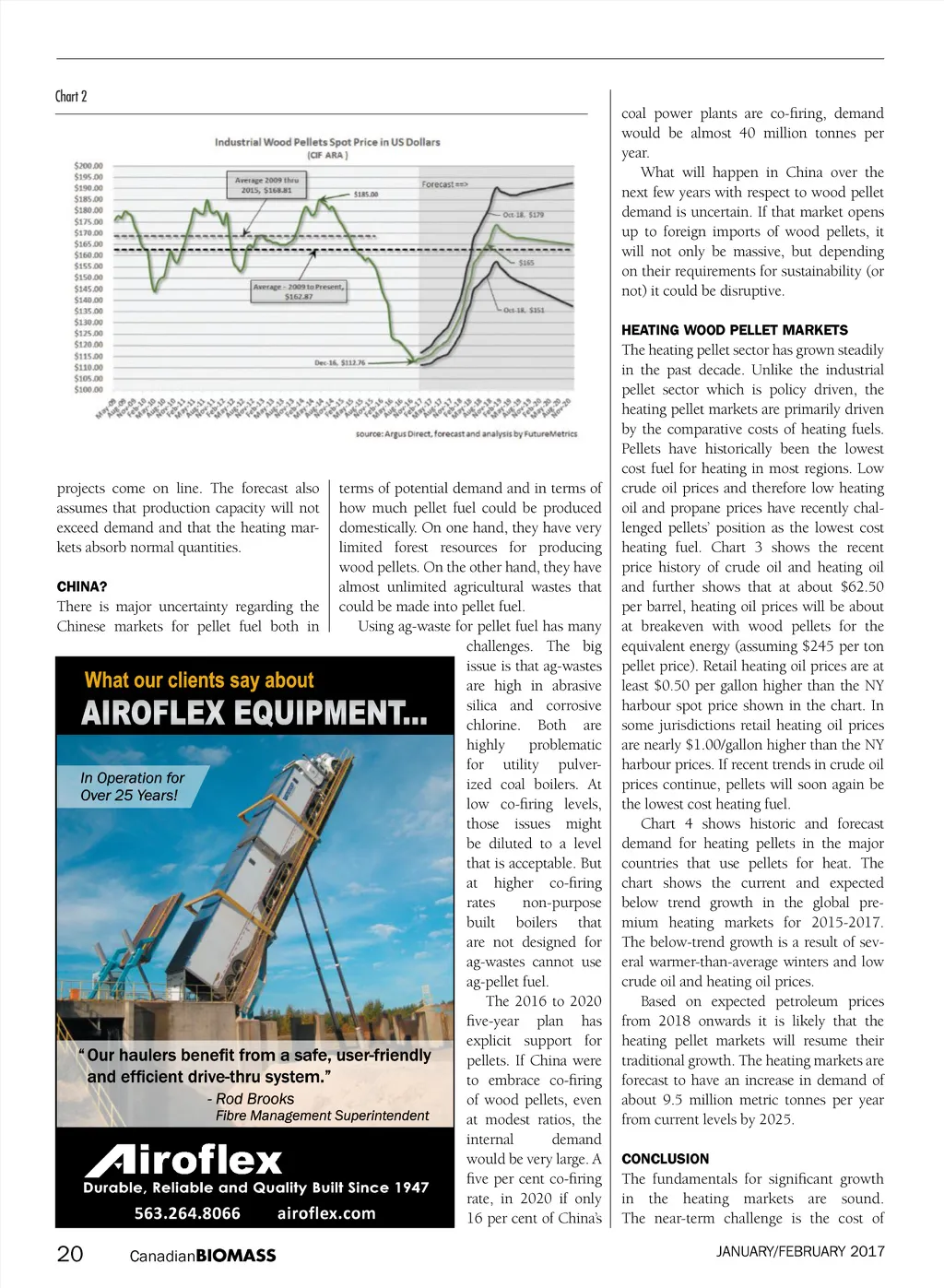

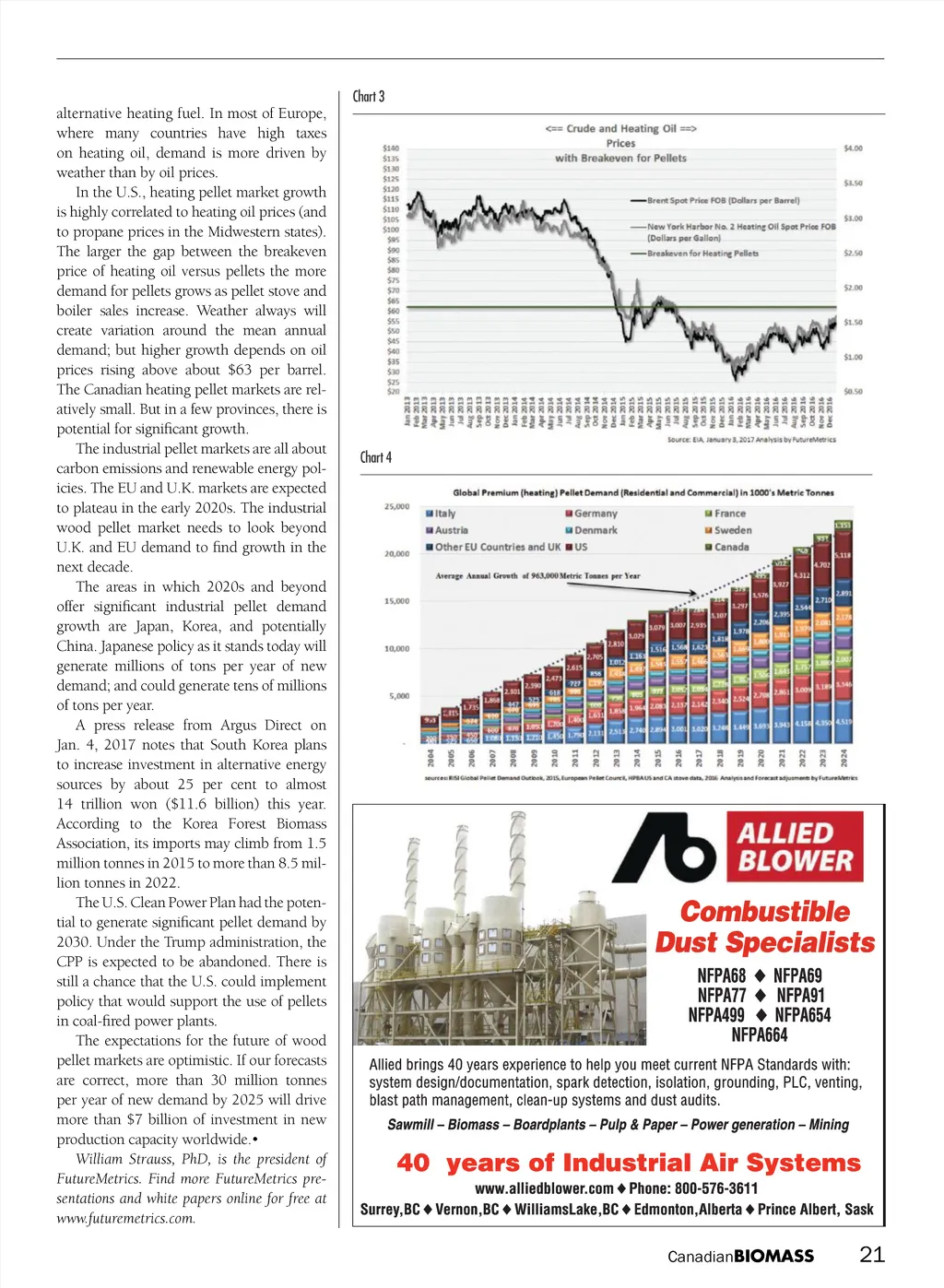

Chart 2 coal power plants are co-firing, demand would be almost 40 million tonnes per year. What will happen in China over the next few years with respect to wood pellet demand is uncertain. If that market opens up to foreign imports of wood pellets, it will not only be massive, but depending on their requirements for sustainability (or not) it could be disruptive. HEATING WOOD PELLET MARKETS terms of potential demand and in terms of how much pellet fuel could be produced domestically. On one hand, they have very limited forest resources for producing wood pellets. On the other hand, they have almost unlimited agricultural wastes that CHINA? There is major uncertainty regarding the could be made into pellet fuel. Using ag-waste for pellet fuel has many Chinese markets for pellet fuel both in challenges. The big issue is that ag-wastes are high in abrasive silica and corrosive chlorine. Both are highly problematic for utility pulver-ized coal boilers. At low co-firing levels, those issues might be diluted to a level that is acceptable. But at higher co-firing rates non-purpose built boilers that are not designed for ag-wastes cannot use ag-pellet fuel. The 2016 to 2020 five-year plan has explicit support for pellets. If China were to embrace co-firing of wood pellets, even at modest ratios, the internal demand would be very large. A five per cent co-firing rate, in 2020 if only 563.264.8066 airoflex.com 16 per cent of China’s projects come on line. The forecast also assumes that production capacity will not exceed demand and that the heating mar-kets absorb normal quantities. The heating pellet sector has grown steadily in the past decade. Unlike the industrial pellet sector which is policy driven, the heating pellet markets are primarily driven by the comparative costs of heating fuels. Pellets have historically been the lowest cost fuel for heating in most regions. Low crude oil prices and therefore low heating oil and propane prices have recently chal-lenged pellets’ position as the lowest cost heating fuel. Chart 3 shows the recent price history of crude oil and heating oil and further shows that at about $62.50 per barrel, heating oil prices will be about at breakeven with wood pellets for the equivalent energy (assuming $245 per ton pellet price). Retail heating oil prices are at least $0.50 per gallon higher than the NY harbour spot price shown in the chart. In some jurisdictions retail heating oil prices are nearly $1.00/gallon higher than the NY harbour prices. If recent trends in crude oil prices continue, pellets will soon again be the lowest cost heating fuel. Chart 4 shows historic and forecast demand for heating pellets in the major countries that use pellets for heat. The chart shows the current and expected below trend growth in the global pre-mium heating markets for 2015-2017. The below-trend growth is a result of sev-eral warmer-than-average winters and low crude oil and heating oil prices. Based on expected petroleum prices from 2018 onwards it is likely that the heating pellet markets will resume their traditional growth. The heating markets are forecast to have an increase in demand of about 9.5 million metric tonnes per year from current levels by 2025. CONCLUSION The fundamentals for significant growth in the heating markets are sound. The near-term challenge is the cost of JANUARY/FEBRUARY 2017 20 Canadian BIOMASS

Canadian Biomass January February 2017: Page 20