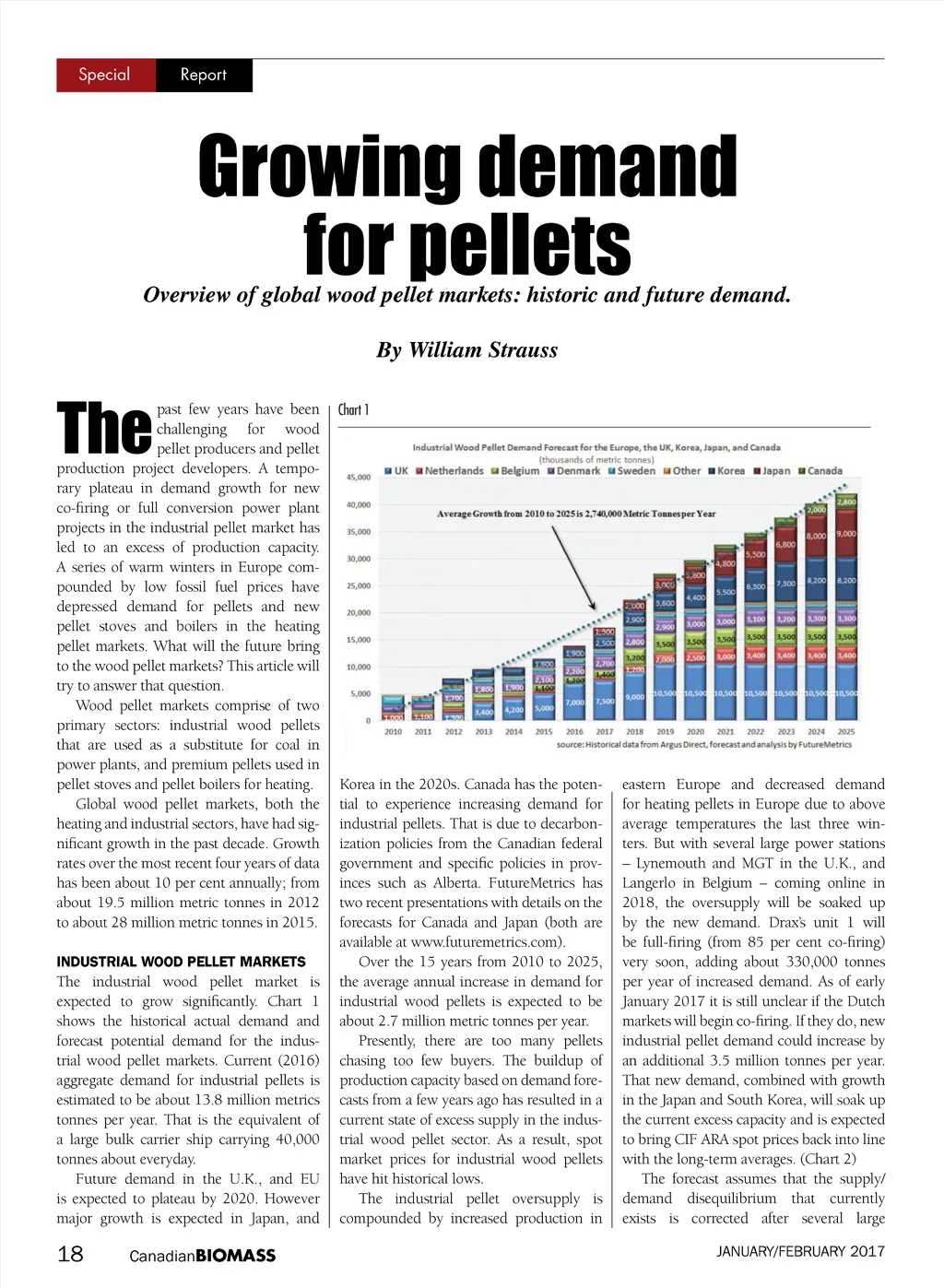

Special Report Overview of global wood pellet markets: historic and future demand. By William Strauss Growing demand for pellets Chart 1 The past few years have been challenging for wood pellet producers and pellet production project developers. A tempo-rary plateau in demand growth for new co-firing or full conversion power plant projects in the industrial pellet market has led to an excess of production capacity. A series of warm winters in Europe com-pounded by low fossil fuel prices have depressed demand for pellets and new pellet stoves and boilers in the heating pellet markets. What will the future bring to the wood pellet markets? This article will try to answer that question. Wood pellet markets comprise of two primary sectors: industrial wood pellets that are used as a substitute for coal in power plants, and premium pellets used in pellet stoves and pellet boilers for heating. Global wood pellet markets, both the heating and industrial sectors, have had sig-nificant growth in the past decade. Growth rates over the most recent four years of data has been about 10 per cent annually; from about 19.5 million metric tonnes in 2012 to about 28 million metric tonnes in 2015. INDUSTRIAL WOOD PELLET MARKETS The industrial wood pellet market is expected to grow significantly. Chart 1 shows the historical actual demand and forecast potential demand for the indus-trial wood pellet markets. Current (2016) aggregate demand for industrial pellets is estimated to be about 13.8 million metrics tonnes per year. That is the equivalent of a large bulk carrier ship carrying 40,000 tonnes about everyday. Future demand in the U.K., and EU is expected to plateau by 2020. However major growth is expected in Japan, and Korea in the 2020s. Canada has the poten-tial to experience increasing demand for industrial pellets. That is due to decarbon-ization policies from the Canadian federal government and specific policies in prov-inces such as Alberta. FutureMetrics has two recent presentations with details on the forecasts for Canada and Japan (both are available at www.futuremetrics.com). Over the 15 years from 2010 to 2025, the average annual increase in demand for industrial wood pellets is expected to be about 2.7 million metric tonnes per year. Presently, there are too many pellets chasing too few buyers. The buildup of production capacity based on demand fore-casts from a few years ago has resulted in a current state of excess supply in the indus-trial wood pellet sector. As a result, spot market prices for industrial wood pellets have hit historical lows. The industrial pellet oversupply is compounded by increased production in eastern Europe and decreased demand for heating pellets in Europe due to above average temperatures the last three win-ters. But with several large power stations – Lynemouth and MGT in the U.K., and Langerlo in Belgium – coming online in 2018, the oversupply will be soaked up by the new demand. Drax’s unit 1 will be full-firing (from 85 per cent co-firing) very soon, adding about 330,000 tonnes per year of increased demand. As of early January 2017 it is still unclear if the Dutch markets will begin co-firing. If they do, new industrial pellet demand could increase by an additional 3.5 million tonnes per year. That new demand, combined with growth in the Japan and South Korea, will soak up the current excess capacity and is expected to bring CIF ARA spot prices back into line with the long-term averages. (Chart 2) The forecast assumes that the supply/ demand disequilibrium that currently exists is corrected after several large JANUARY/FEBRUARY 2017 18 Canadian BIOMASS

Canadian Biomass January February 2017: Page 18