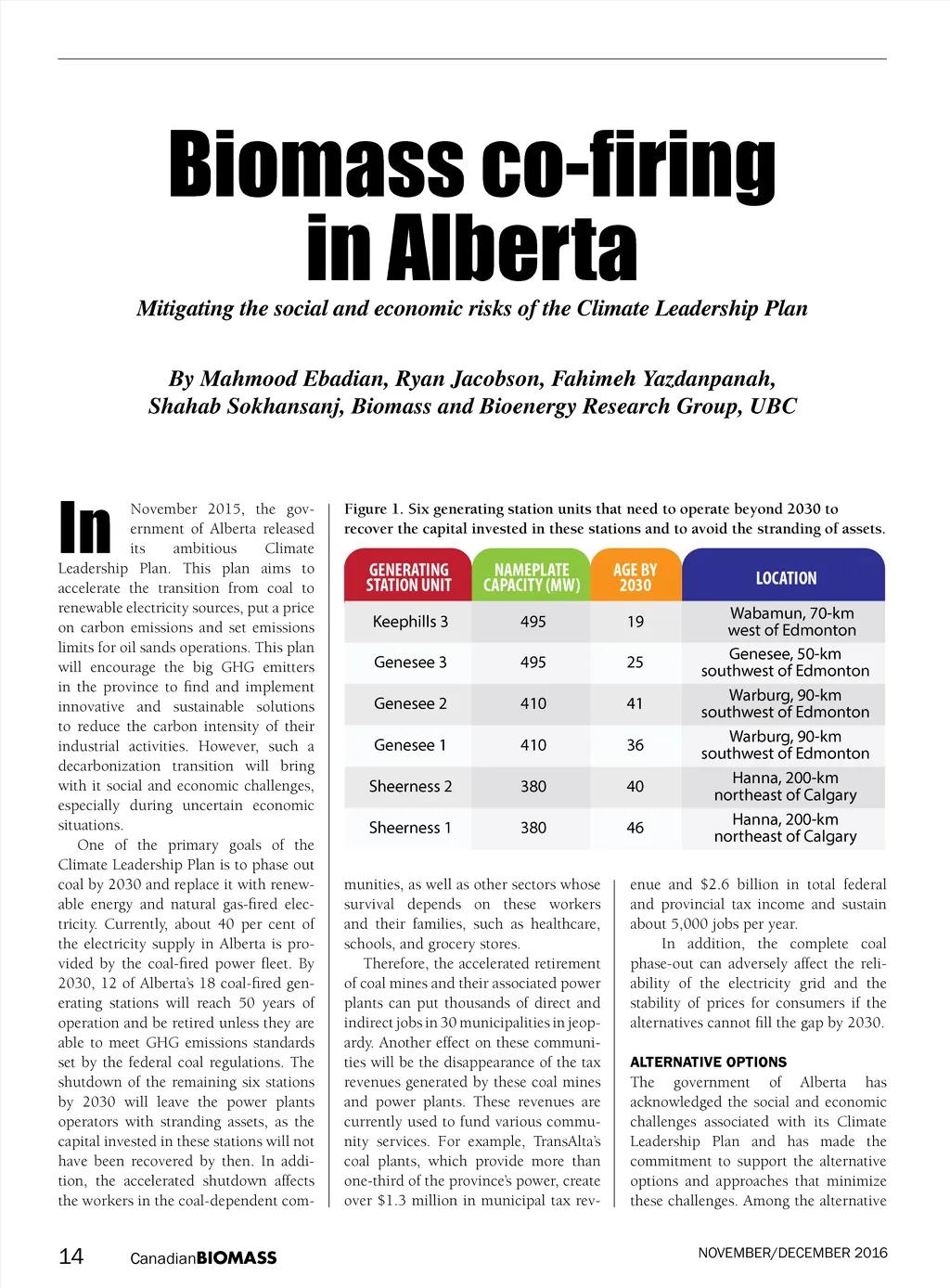

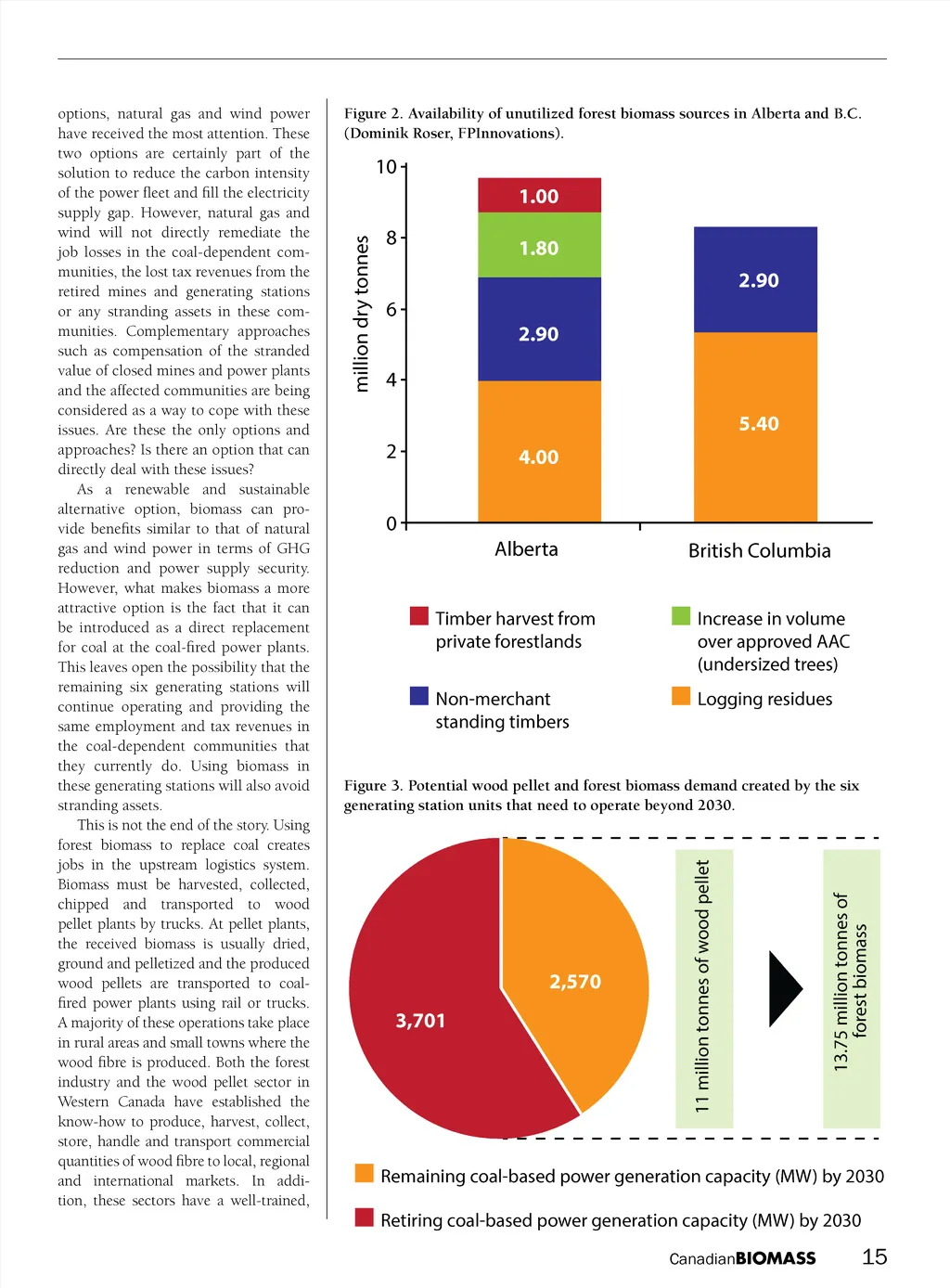

ta Columbia0000 fromands t ers options, natural gas and wind power have received the most attention. These two options are certainly part of the solution to reduce the carbon intensity of the power fleet and fill the electricity supply gap. However, natural gas and wind will not directly remediate the job losses in the coal-dependent com-munities, the lost tax revenues from the retired mines and generating stations or any stranding assets in these com-munities. Complementary approaches such as compensation of the stranded value of closed mines and power plants and the affected communities are being considered as a way to cope with these issues. Are these the only options and approaches? Is there an option that can directly deal with these issues? 5.40 As a renewable and sustainable alternative option, biomass can pro-vide benefits similar to that of natural gas and wind power in terms of GHG reduction and power supply security. However, what makes biomass a more British attractive option is the fact that it can be introduced as a direct replacement for coal at the coal-fired power plants. This leaves open the possibility that the Increase in volume remaining six generating stations will over approved AAC continue operating and providing the (undersized trees) in same employment and tax revenues the coal-dependent communities that Logging residues they currently do. Using biomass in these generating stations will also avoid stranding assets. This is not the end of the story. Using forest biomass to replace coal creates jobs in the upstream logistics system. Biomass must be harvested, collected, chipped and transported to wood pellet plants by trucks. At pellet plants, the received biomass is usually dried, ground and pelletized and the produced wood pellets are transported to coal-fired power plants using rail or trucks. A majority of these operations take place in rural areas and small towns where the wood fibre is produced. Both the forest industry and the wood pellet sector in Western Canada have established the know-how to produce, harvest, collect, store, handle and transport commercial quantities of wood fibre to local, regional and international markets. In addi-tion, these sectors have a well-trained, Figure 2. Availability of unutilized forest biomass sources in Alberta and B.C. (Dominik Roser, FPInnovations). 10 1.00 million dry tonnes 8 6 4 1.80 2.90 2.90 2.90st 5.40 2 0 Alberta Timber harvest from private forestlands Non-merchant standing timbers 4.00 British Columbia Increase in volume over approved AAC (undersized trees) Logging residues Figure 3. Potential wood pellet and forest biomass demand created by the six generating station units that need to operate beyond 2030. 11 million tonnes of wood pellet 13.75 million tonnes of forest biomass 2,570 3,701 3 Rem Remaining coal-based power generation capacity (MW) by 2030 Retiring coal-based power generation capacity (MW) by 2030 Canadian BIOMASS Ret 15

Canadian Biomass November December 2016: Page 15