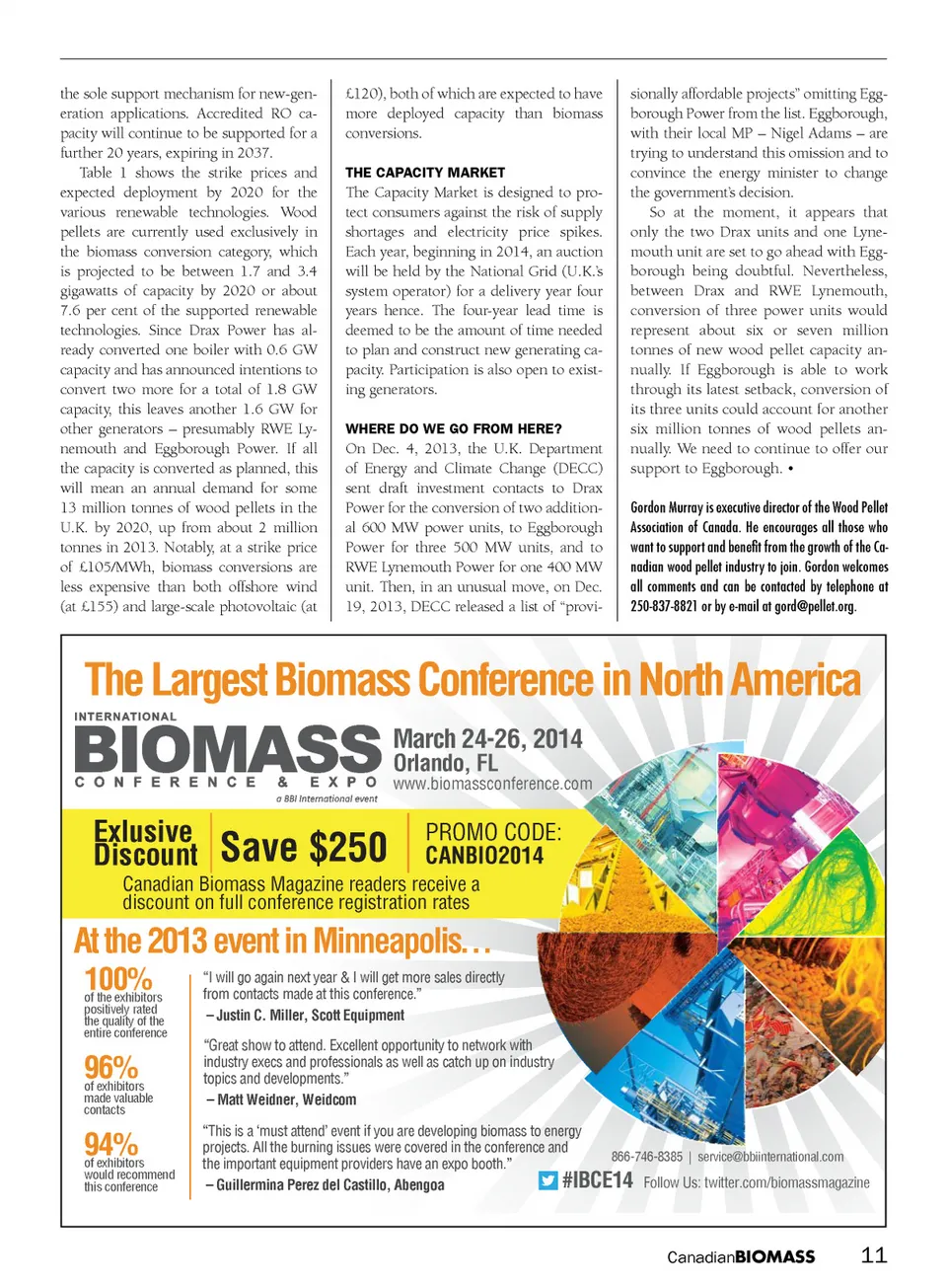

WPAC Report U.K. energy Act receives royal assent Electricity market reform to provide huge boost to wood pellet industry. By Gordon Murray he U.K. Energy Act received royal assent from the Queen on Dec. 18, 2013. This was the culmination of a long process, which began as a govern-ment consultation in December 2010. The consultation led to a White Paper on Electricity Market Reform in July 2011, which in turn became the draft Energy Bill. The Energy Bill was introduced to Parliament in November 2012, and after much debate, finally became law in De-cember 2013. Of particular interest to wood pellet producers is that the Act provides for Electricity Market Reform (EMR). The government is required to publish an EMR Delivery Plan every five years and the first such plan was delivered on Dec. 19, 2013, just one day after Act became law. The government’s EMR objectives are: (1) to ensure a secure electricity supply through sufficient capacity to meet any demand, a diverse portfolio of generation technologies and a reduced reliance on fossil fuels; (2) to ensure sufficient in-vestment in sustainable low-carbon tech-nologies to provide the necessary sup-port and stable revenues to decarbonize electricity generation; and (3) to do so in a way which maximizes benefits and minimizes costs to the U.K. economy and to taxpayers and consumers. The government will meet its EMR objectives by using two mechanisms: Contracts for Difference (CfDs) and the Capacity Market. These mechanisms will be supported by: • A tax on fossil fuels used to gen-erate electricity; • Limiting CO2 emissions from fossil fuel power stations; • Incentivizing electricity demand t • reduction; and Supporting market liquidity and access to market for independent renewable generators. ContraCts for DifferenCe CfDs will support low-carbon generation by giving eligible generators increased price certainty through a long-term con-tract. A CfD will largely remove exposure to volatile wholesale prices during the CfD period, reducing investment risk. Generators will receive revenue from selling their electricity into the market as usual and will also receive a top-up to a pre agreed “strike price.” If the market price is greater than the strike price, the generator must pay back the difference. CfDs will operate alongside the Renew-ables Obligation (RO), which is the ex-isting support scheme for large-scale renewable generation. The strike prices for initial EMR period have been set so that they are broadly comparable to the levels of support available under the RO, adjusted to account for the greater reve-nue certainty and shorter contract length provided by a CfD. In aggregate, consum-ers pay less under the CfD than under the RO as CfDs will reduce the risks faced by generators and improve the stability of their revenues. There will be a transition period until March 31, 2017, during which the RO and CfD will both be open for applica-tions from new renewable generating ca-pacity. On March 31, 2017, the RO will close to new capacity and the CfD will be table 1. renewable energy strike PriCes anD ProjeCteD DePloyment 2014/15 Strike price – £/MWh Advanced Conversion Technologies Anaerobic Digestion Biomass Conversion Dedicated Biomass with CHP Energy from Waste with CHP Geothermal Hydro Landfill Gas Offshore Wind Onshore Wind Sewage Gas Large Scale Photovoltaic Tidal Stream and Wave 155 150 105 125 80 145 100 55 155 95 75 120 305 Deployment by 2020 – GW 0.2 -0.3 0.3 -0.4 1.7 -3.4 0.3 -0.6 0.4 <0.1 1.7 0.9 8 -15 11 -13 0.2 2.4 -4 0.1 Deployment – % 0.7% 1.0% 7.6% 1.3% 1.2% 0.0% 5.1% 2.7% 34.2% 35.7% 0.6% 9.5% 0.3% 10 Canadian BIOMASS January/February 2014

Canadian Biomass January/February 2014: Page 10