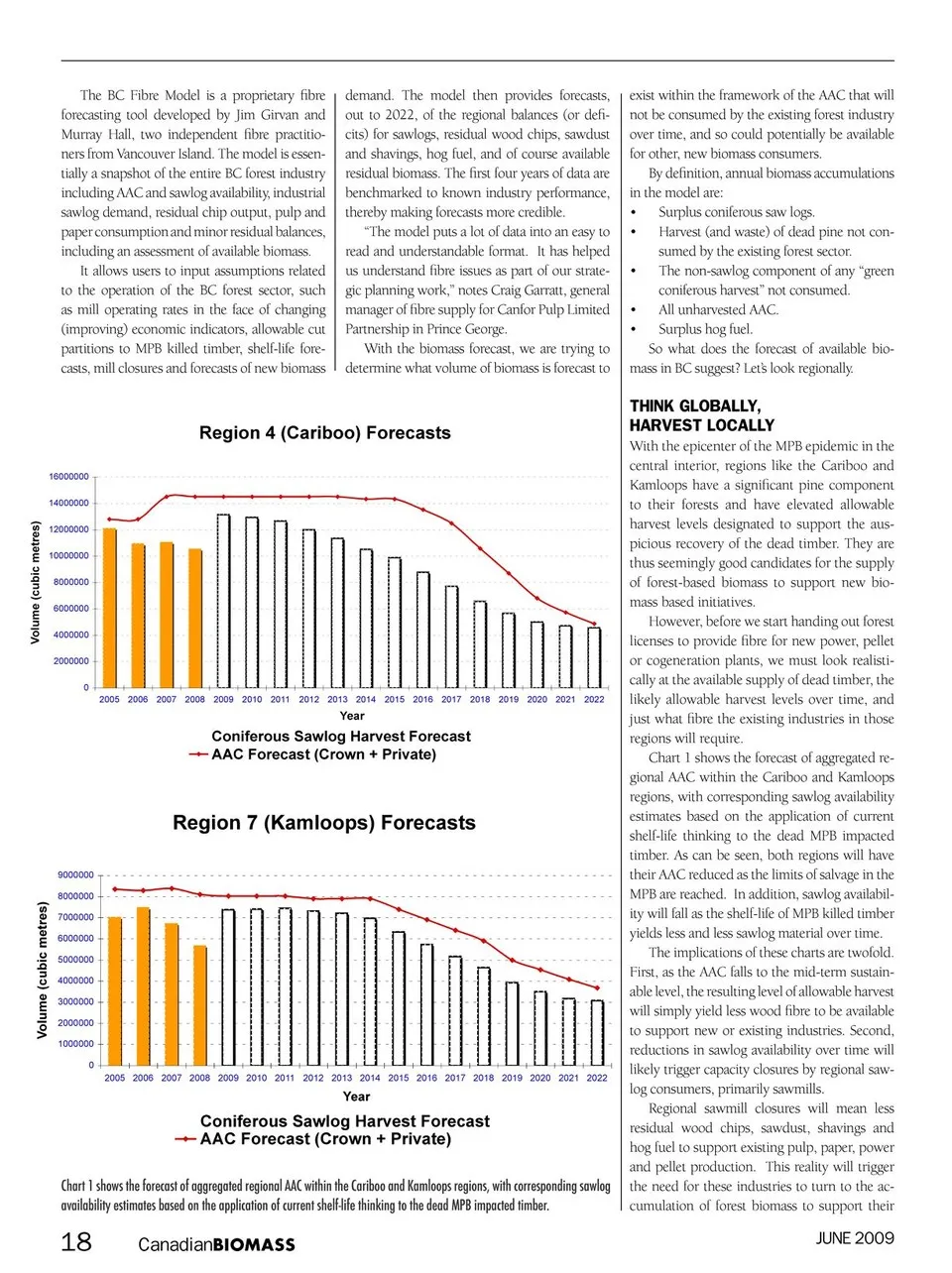

The BC Fibre Model is a proprietary fibre forecasting tool developed by Jim Girvan and Murray Hall, two independent fibre practitio- ners from Vancouver Island. The model is essen- tially a snapshot of the entire BC forest industry including AAC and sawlog availability, industrial sawlog demand, residual chip output, pulp and paper consumption and minor residual balances, including an assessment of available biomass. It allows users to input assumptions related to the operation of the BC forest sector, such as mill operating rates in the face of changing (improving) economic indicators, allowable cut partitions to MPB killed timber, shelf-life fore- casts, mill closures and forecasts of new biomass demand. The model then provides forecasts, out to 2022, of the regional balances (or defi- cits) for sawlogs, residual wood chips, sawdust and shavings, hog fuel, and of course available residual biomass. The first four years of data are benchmarked to known industry performance, thereby making forecasts more credible. “The model puts a lot of data into an easy to read and understandable format. It has helped us understand fibre issues as part of our strate- gic planning work,” notes Craig Garratt, general manager of fibre supply for Canfor Pulp Limited Partnership in Prince George. With the biomass forecast, we are trying to determine what volume of biomass is forecast to Region 4 (Cariboo) Forecasts 10000000 12000000 14000000 16000000 2000000 4000000 6000000 8000000 0 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 Year Coniferous Sawlog Harvest Forecast AAC Forecast (Crown + Private) Region 7 (Kamloops) Forecasts 1000000 2000000 3000000 4000000 5000000 6000000 7000000 8000000 9000000 0 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 Year Coniferous Sawlog Harvest Forecast AAC Forecast (Crown + Private) Chart 1 shows the forecast of aggregated regional AAC within the Cariboo and Kamloops regions, with corresponding sawlog availability estimates based on the application of current shelf-life thinking to the dead MPB impacted timber. 18 CanadianBIOMASS exist within the framework of the AAC that will not be consumed by the existing forest industry over time, and so could potentially be available for other, new biomass consumers. By definition, annual biomass accumulations in the model are: • Surplus coniferous saw logs. • Harvest (and waste) of dead pine not con- sumed by the existing forest sector. • The non-sawlog component of any “green coniferous harvest” not consumed. • All unharvested AAC. • Surplus hog fuel. So what does the forecast of available bio- mass in BC suggest? Let’s look regionally. think gloBally, harveSt locally With the epicenter of the MPB epidemic in the central interior, regions like the Cariboo and Kamloops have a significant pine component to their forests and have elevated allowable harvest levels designated to support the aus- picious recovery of the dead timber. They are thus seemingly good candidates for the supply of forest-based biomass to support new bio- mass based initiatives. However, before we start handing out forest licenses to provide fibre for new power, pellet or cogeneration plants, we must look realisti- cally at the available supply of dead timber, the likely allowable harvest levels over time, and just what fibre the existing industries in those regions will require. Chart 1 shows the forecast of aggregated re- gional AAC within the Cariboo and Kamloops regions, with corresponding sawlog availability estimates based on the application of current shelf-life thinking to the dead MPB impacted timber. As can be seen, both regions will have their AAC reduced as the limits of salvage in the MPB are reached. In addition, sawlog availabil- ity will fall as the shelf-life of MPB killed timber yields less and less sawlog material over time. The implications of these charts are twofold. First, as the AAC falls to the mid-term sustain- able level, the resulting level of allowable harvest will simply yield less wood fibre to be available to support new or existing industries. Second, reductions in sawlog availability over time will likely trigger capacity closures by regional saw- log consumers, primarily sawmills. Regional sawmill closures will mean less residual wood chips, sawdust, shavings and hog fuel to support existing pulp, paper, power and pellet production. This reality will trigger the need for these industries to turn to the ac- cumulation of forest biomass to support their JUNE 2009 Volume (cubic metres) Volume (cubic metres)

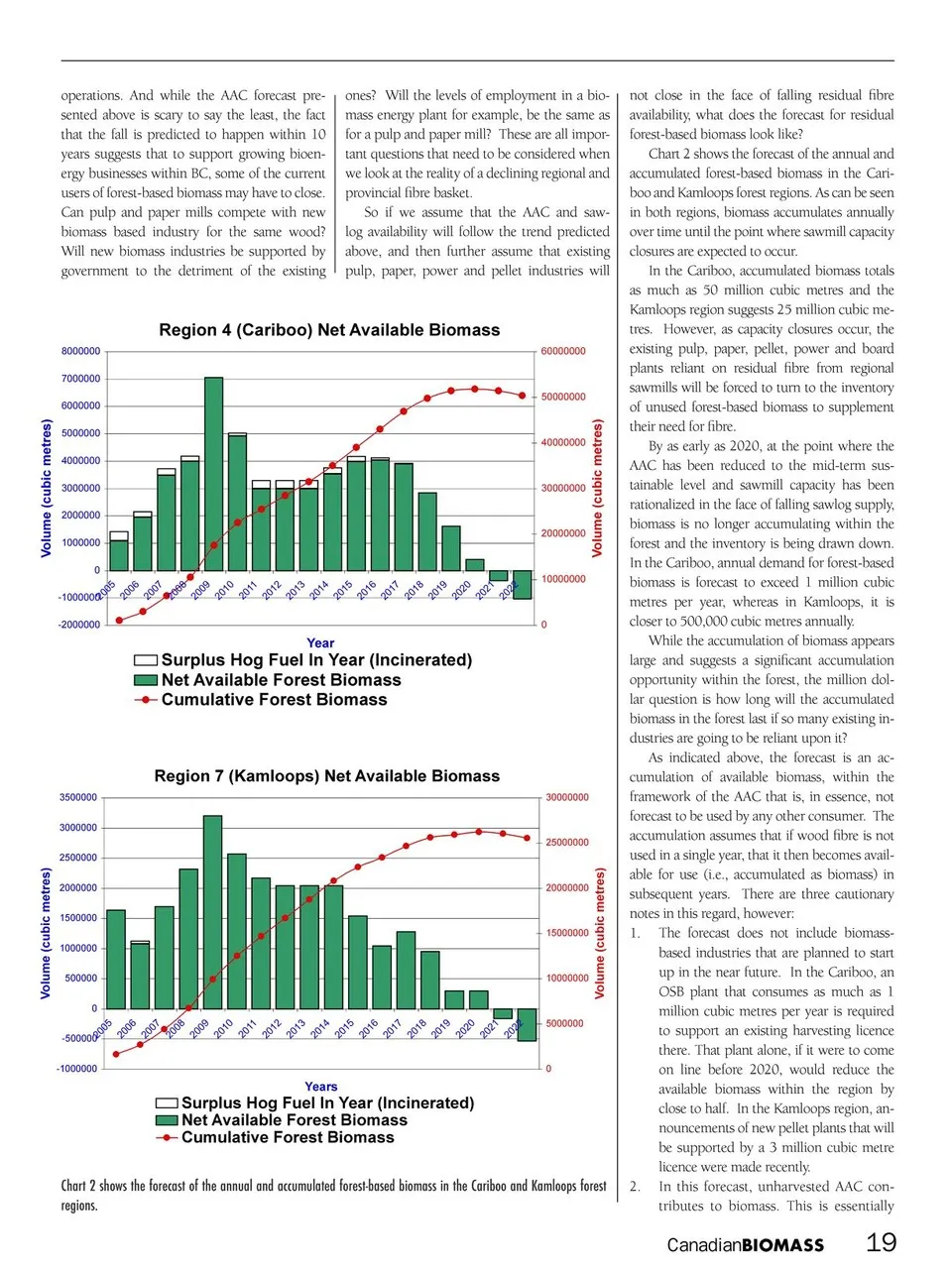

Canadian Biomass June 2009: Page 18