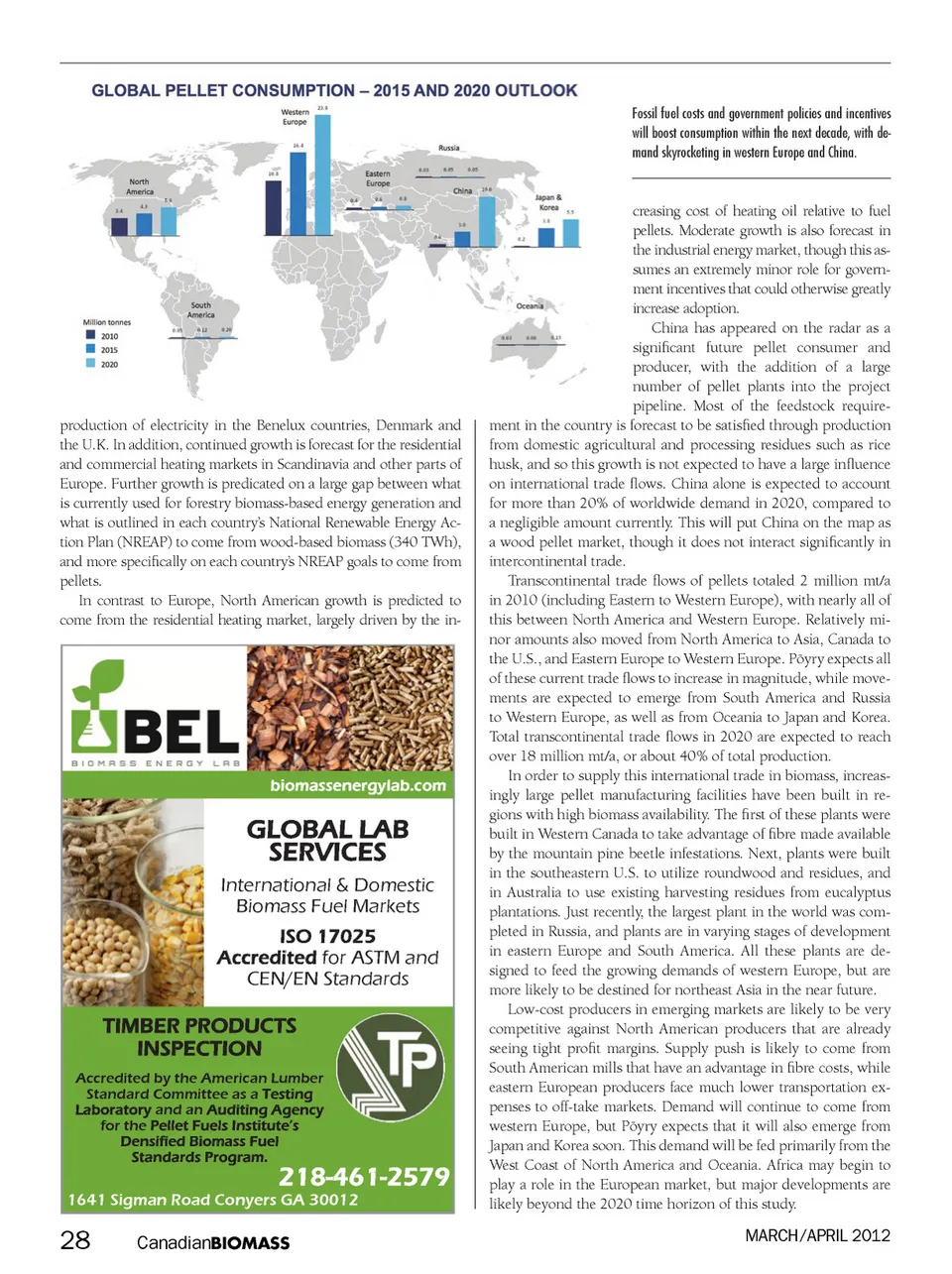

The other side of the pellet industry is the residential market. This facet is highly fragmented in most regions. These smaller plants vastly outnumber larger indus-trial ones, since they often utilize sawmill residues from nearby wood products in-dustries or are integrated directly into a sawmill. Because of the various markets to which these residues can be sold, and fluctuations in wood product demand and sawlog supply, many of these facilities of-ten run at low utilization rates. This was very much the case during the econom-ic downturn of the previous two years, where all wood product manufacturing decreased and fewer residues were avail-able to the market. Couple this to the fact that a significant number of pellet manu-facturing facilities focusing on the resi-dential markets came online in 2008 and 2009, it becomes clear that currently this can be a difficult market to be in. Production conditions and end-use markets for the two different pellet classes differ, as do their prices and respective outlooks. Residential pellet markets are usually rather regional and are expected to remain this way, though prices are expect-ed to increase in Europe (where the great-est number of trades occur). Industrial pellet prices are more reminiscent of com-modities, and are therefore less regional. Pöyry predicts that the prices for the lat-ter will remain relatively stable thanks to the large amounts of supply that will come online from new regions, while incentives in Europe will both increase demand and act as a sort of cap on what pellet consum-ers are able to pay. The magnitude of growth for this mar-ket is heavily dependent on the political will for expanding biomass energy utilization and the associated incentives surrounding it. These incentives are currently especially favourable in countries such as the Nether-lands, Denmark, Belgium and the United Kingdom. In addition, demand depends on the cost of alternative energy sources to pel-lets, which influences the competitiveness of such a fuel. This is especially the case in countries where the bulk of pellet demand is in the residential sector, for example Ger-many and the United States. There are some signs that industrial users of pellets are beginning to integrate upstream by building their own pellet mills in areas with high biomass avail-ability, as is the case with RWE/Georgia Biomass and Vattenfall/Miramichi. This step can assure biomass energy producers better control over supply chains, but not supply security. In addition, many small pellet produc-ers are starting to either downstream inte-grate to control their distribution or join with other pellet producers to increase their market share, at least regionally. This shows signs of market maturation, though in most markets, biomass pellets have not reached the point of being a commodity due to differing quality standards and a lack of transparency from relatively few trades per unit of time. Producers may struggle to keep costs low in order to maintain their bottom line. It will remain essential to find ways to improve efficien-cy and increase productivity in an increas-ingly competitive market. • This article was submitted by Pöyry Man-agement Consulting. KAHL Wood Pelleting Plants Quality worldwide. AMANDUS KAHL GmbH & Co. KG, SARJ Equipment Corp., Mr. Rick B. MacArthur, 29 Golfview Blvd., Bradford, Ontario L3Z 2A6 Phone: 001-905-778-0073, Fax: 001-905-778-9613, [email protected] www.akahl.de Canadian BIOMASS 29

Canadian Biomass March/April 2012: Page 29