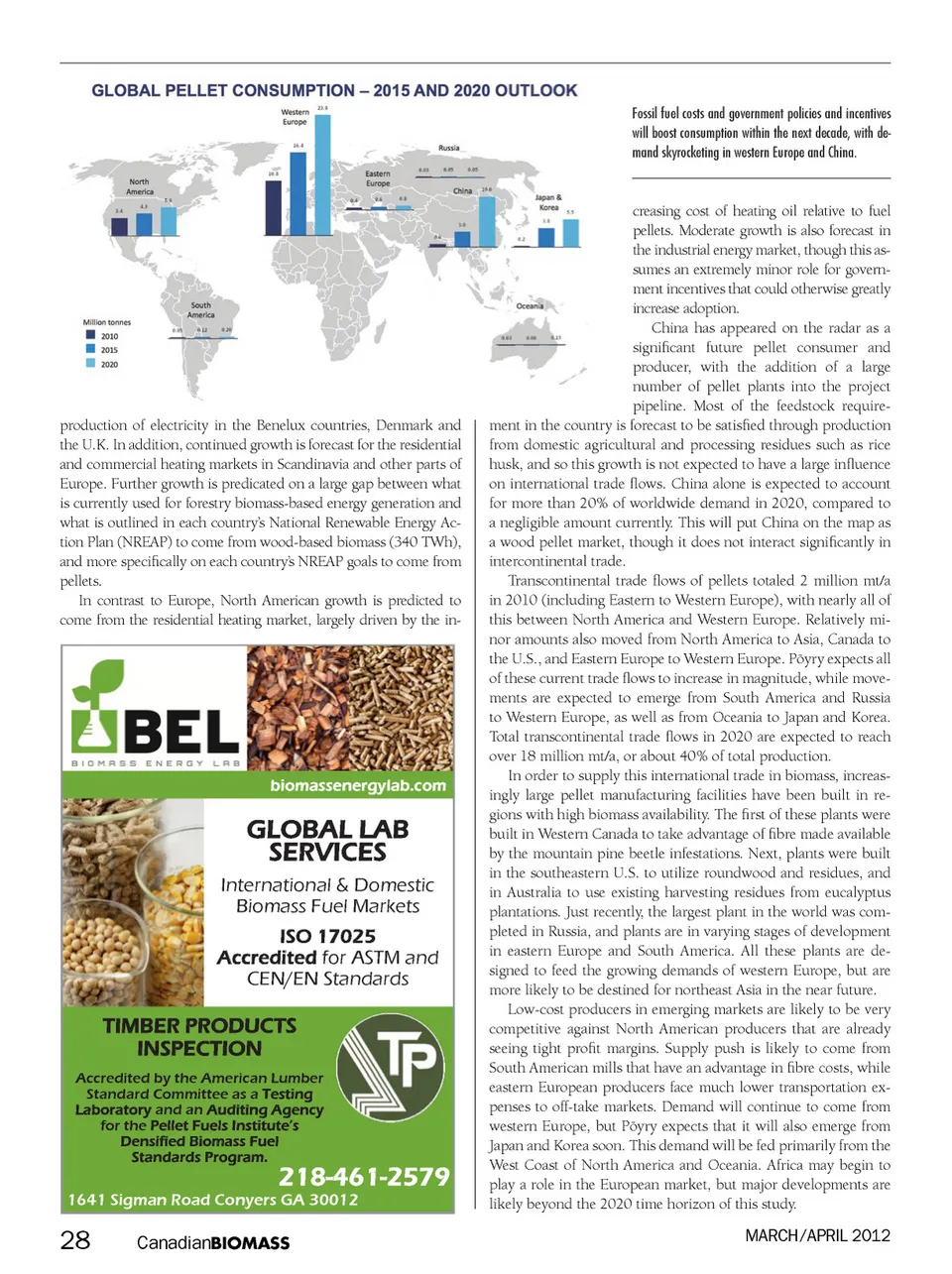

Fossil fuel costs and government policies and incentives will boost consumption within the next decade, with de-mand skyrocketing in western Europe and China. production of electricity in the Benelux countries, Denmark and the U.K. In addition, continued growth is forecast for the residential and commercial heating markets in Scandinavia and other parts of Europe. Further growth is predicated on a large gap between what is currently used for forestry biomass-based energy generation and what is outlined in each country’s National Renewable Energy Ac-tion Plan (NREAP) to come from wood-based biomass (340 TWh), and more specifically on each country’s NREAP goals to come from pellets. In contrast to Europe, North American growth is predicted to come from the residential heating market, largely driven by the in-biomassenergylab.com GLOBAL LAB SERVICES International & Domestic Biomass Fuel Markets ISO 17025 Accredited for ASTM and CEN/EN Standards TIMBER PRODUCTS INSPECTION Accredited by the American Lumber Standard Committee as a Testing Laboratory and an Auditing Agency for the Pellet Fuels Institute’s Densified Biomass Fuel Standards Program. 1641 Sigman Road Conyers GA 30012 218-461-2579 creasing cost of heating oil relative to fuel pellets. Moderate growth is also forecast in the industrial energy market, though this as-sumes an extremely minor role for govern-ment incentives that could otherwise greatly increase adoption. China has appeared on the radar as a significant future pellet consumer and producer, with the addition of a large number of pellet plants into the project pipeline. Most of the feedstock require-ment in the country is forecast to be satisfied through production from domestic agricultural and processing residues such as rice husk, and so this growth is not expected to have a large influence on international trade flows. China alone is expected to account for more than 20% of worldwide demand in 2020, compared to a negligible amount currently. This will put China on the map as a wood pellet market, though it does not interact significantly in intercontinental trade. Transcontinental trade flows of pellets totaled 2 million mt/a in 2010 (including Eastern to Western Europe), with nearly all of this between North America and Western Europe. Relatively mi-nor amounts also moved from North America to Asia, Canada to the U.S., and Eastern Europe to Western Europe. Pöyry expects all of these current trade flows to increase in magnitude, while move-ments are expected to emerge from South America and Russia to Western Europe, as well as from Oceania to Japan and Korea. Total transcontinental trade flows in 2020 are expected to reach over 18 million mt/a, or about 40% of total production. In order to supply this international trade in biomass, increas-ingly large pellet manufacturing facilities have been built in re-gions with high biomass availability. The first of these plants were built in Western Canada to take advantage of fibre made available by the mountain pine beetle infestations. Next, plants were built in the southeastern U.S. to utilize roundwood and residues, and in Australia to use existing harvesting residues from eucalyptus plantations. Just recently, the largest plant in the world was com-pleted in Russia, and plants are in varying stages of development in eastern Europe and South America. All these plants are de-signed to feed the growing demands of western Europe, but are more likely to be destined for northeast Asia in the near future. Low-cost producers in emerging markets are likely to be very competitive against North American producers that are already seeing tight profit margins. Supply push is likely to come from South American mills that have an advantage in fibre costs, while eastern European producers face much lower transportation ex-penses to off-take markets. Demand will continue to come from western Europe, but Pöyry expects that it will also emerge from Japan and Korea soon. This demand will be fed primarily from the West Coast of North America and Oceania. Africa may begin to play a role in the European market, but major developments are likely beyond the 2020 time horizon of this study. MARCH/APRIL 2012 28 Canadian BIOMASS

Canadian Biomass March/April 2012: Page 28